On March 23, Reuters reported that three African countries are in talks on debt-for-nature swaps totalling about $500 million, with one deal potentially closing in 2026 and two more in 2027, according to The Nature Conservancy. On the surface, that can sound like a niche conservation story. It is not. It is a financing story, a sovereign-debt story, and a test of whether African governments can unlock fiscal space by treating natural capital as part of the balance-sheet conversation rather than a side issue for donors and NGOs.

The deeper significance is this: many African states are confronting two pressures at once. First, they are underfunded on climate and resilience. Second, they are still operating in a debt environment where every additional dollar of conventional borrowing is politically and fiscally harder to justify. Debt-for-nature swaps sit in the narrow space between those realities. They do not erase debt crises, and they do not replace broad climate finance. But they may offer a way to refinance part of a country’s obligations while directing savings toward ecosystems that protect coastlines, support fisheries, sustain tourism, preserve forests, and reduce long-run climate vulnerability.

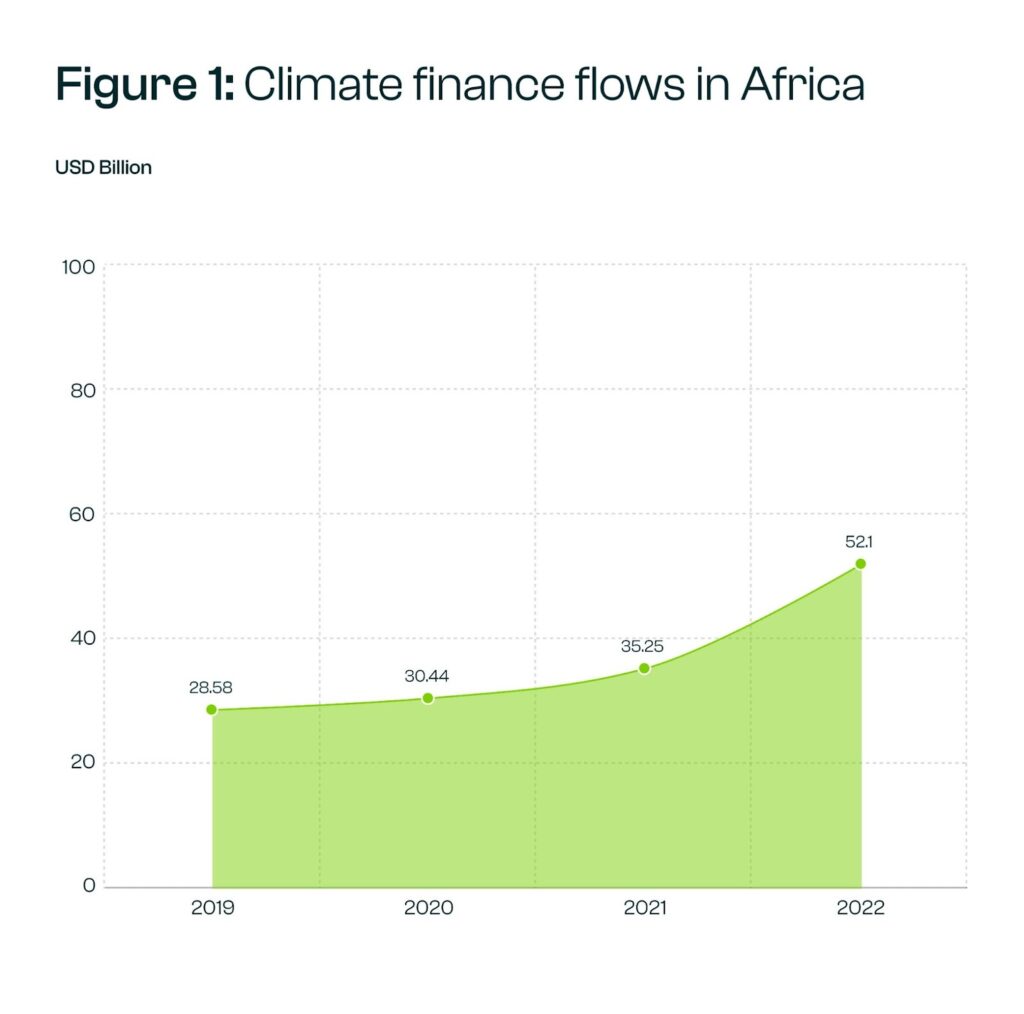

That matters because Africa’s financing gap remains severe, even after recent improvements. Climate Policy Initiative estimates that climate finance flowing into Africa rose 48%, from $29.5 billion in 2019/20 to $43.7 billion in 2021/22, and that annual flows crossed $52.1 billion in 2022 for the first time. Yet the same CPI work shows that Africa still received only 3.3% of global climate finance flows in 2021/22.

Its earlier 2022 work estimated that the continent would need $277 billion annually to meet its 2030 climate goals, while its 2024 report says Africa’s climate finance needs are now roughly $190 billion per year through 2030. The change in the number is not evidence that the problem got smaller. It reflects changing methodologies, updated country plans, and the difficulty of consistently measuring adaptation needs. The honest conclusion is that, whether one uses the lower or the higher estimate, the gap remains massive.

Adaptation alone underscores the scale of the challenge. CPI and the Global Centre on Adaptation estimate Africa needs more than $50 billion a year for adaptation, around 2.5% of GDP, and put adaptation needs at about $52.7 billion annually through 2035 based on available NDC data. Yet Africa received only about $11.4 billion annually in adaptation finance in 2019-2020, and even that estimate is likely conservative because many countries do not cost their adaptation plans comprehensively. This is one of the core reasons debt-for-nature swaps are back on the table. They are not being considered in a vacuum. They are being reconsidered because conventional flows are not remotely matching the scale of climate exposure.

At the same time, debt pressures are narrowing the room to manoeuvre. The IMF’s October 2025 Regional Economic Outlook says Sub-Saharan Africa is still projected to grow 4.1% in 2025, but it also warns that rising debt service costs are crowding out development spending and that macroeconomic vulnerabilities remain high. The World Bank’s latest debt data show developing countries paid a record $1.4 trillion to service foreign debt in 2023, while IDA-eligible countries paid $96.2 billion, including a record $34.6 billion in interest. OECD data add another layer: in 2023, a record 54 developing countries, nearly half of them in Africa, had net interest payments exceeding 10% of government revenues. This is the backdrop against which any “innovative” financing idea must be judged. If it cannot create meaningful fiscal breathing room, it risks becoming a headline rather than a solution.

So what exactly is a debt-for-nature swap?

In its simplest form, expensive existing debt is bought back or refinanced and replaced with cheaper debt, often with support from a multilateral development bank or political risk insurer.

Because the new structure is safer for investors, borrowing costs fall. Part of the resulting savings is then committed to conservation or climate-related programs under a monitored framework. Reuters’ 2023 explainer on Gabon put it plainly: a country’s government bonds or loans are bought up and replaced with cheaper ones, usually with the help of a development-bank credit guarantee, and the savings are directed toward environmental projects. The mechanism is financial engineering with a policy condition attached.

This instrument is not theoretical. It has already been used in multiple sovereign transactions. Reuters’ December 2024 review lists the Seychelles deal in 2016, which bought back $21.6 million of Paris Club debt; Belize in 2021, where a $533 million bond was bought back and retired, delivering about $200 million in debt relief; Barbados in 2022 with a $150 million conversion and again in 2024 with an almost $300 million resilience-focused deal; Ecuador in 2023 with a $1.6 billion buyback tied to Galapagos conservation; Gabon in 2023 with a new $500 million blue bond used to buy back $436 million of international bonds; The Bahamas in 2024 with a $300 million swap unlocking more than $120 million; and El Salvador in 2024, which used a $1 billion loan-backed structure to free up $352 million for watershed conservation. These cases vary in design and ambition, but together they show that the market is no longer experimental. It is maturing into a recognised, if still specialised, financing category.

For Africa, Gabon is the most important precedent.

The Nature Conservancy says the 2023 transaction refinanced part of Gabon’s debt through a $500 million blue bond and is expected to unlock $163 million for marine conservation over 15 years. Reuters similarly reported that the structure helped free up around $163 million while backing Gabon’s commitment to protect 30% of its coastal waters. The symbolic importance here is hard to miss. Gabon became the first country in mainland Africa to complete this type of deal, proving that the model can move beyond island states and Latin American showcases.

The new Reuters report suggests that Gabon may no longer be an exception. In September 2024, Reuters had already reported that at least five African countries were exploring what could become the world’s first joint debt-for-nature swap, aimed at raising at least $2 billion for a coral-rich stretch of the Indian Ocean under the Great Blue Wall initiative. That proposal was designed to help restore 2 million hectares of ocean ecosystems by 2030 and benefit 70 million coastal residents.

Today’s three-country, $500 million pipeline is smaller and more immediate. Still, it fits the same broader pattern: African countries are looking for ways to translate ecological assets into cheaper financing and more resilient public spending.

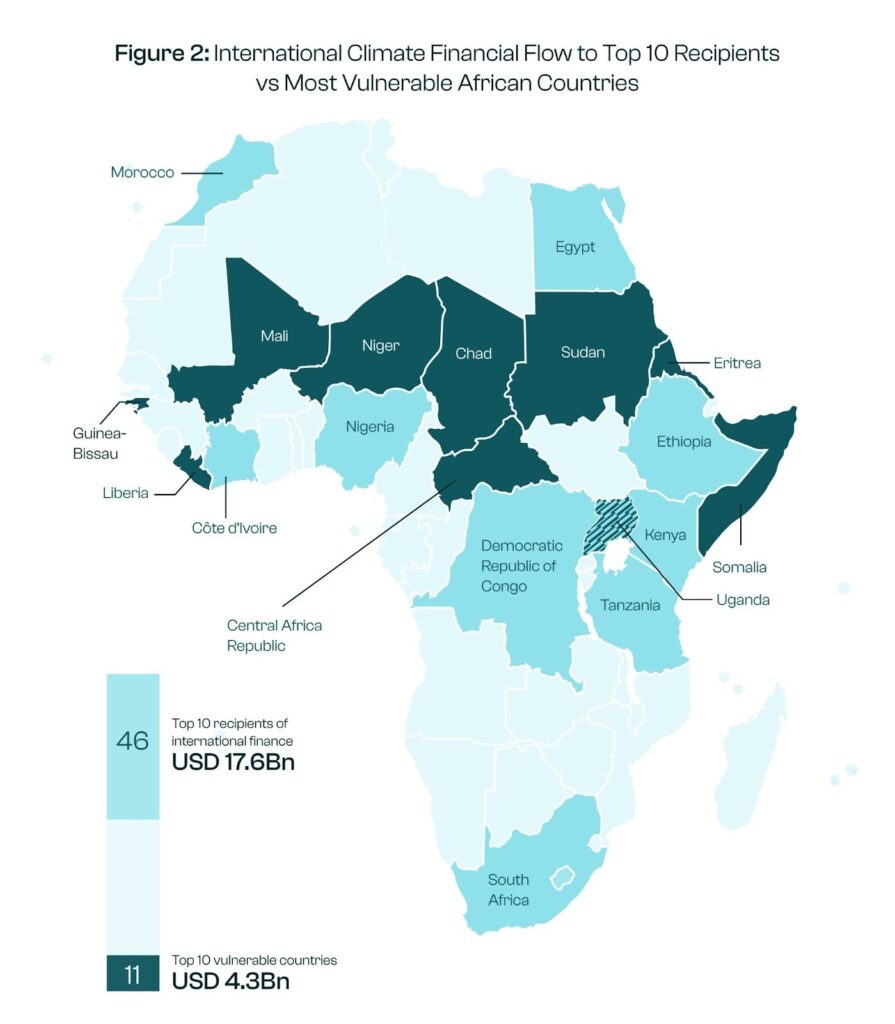

There is a serious strategic logic to this. Africa is rich in natural capital, not poor in it. CPI cites African Development Bank estimates that the continent’s natural capital was worth about $6.2 trillion in 2018. It also notes that climate finance is distributed very unevenly: the top ten recipient countries receive 46% of international climate finance flowing to Africa. In comparison, the ten most climate-vulnerable countries receive only 11%.

In other words, there is both a quantity problem and an allocation problem. Debt-for-nature swaps, if well-designed, could help direct financing toward countries with valuable ecosystems and fiscal constraints that make standard climate investments especially difficult.

But this is where the analysis needs discipline. It would be a mistake to oversell the instrument. OECD warns that debt-for-nature swaps could, in aggregate, help redirect $100 billion of debt in developing countries toward nature restoration and climate adaptation, including $33.7 billion for least developed countries. That sounds large until one remembers the scale of the wider debt problem. The same OECD analysis says transaction-related costs can consume 40% or more of the financial benefits, and it explicitly warns about the relatively small scale of these deals compared with countries’ overall debt burdens, as well as the conditionality and governance demands they impose. That critique matters. A country can complete a swap, receive glowing headlines, and remain fundamentally debt-constrained.

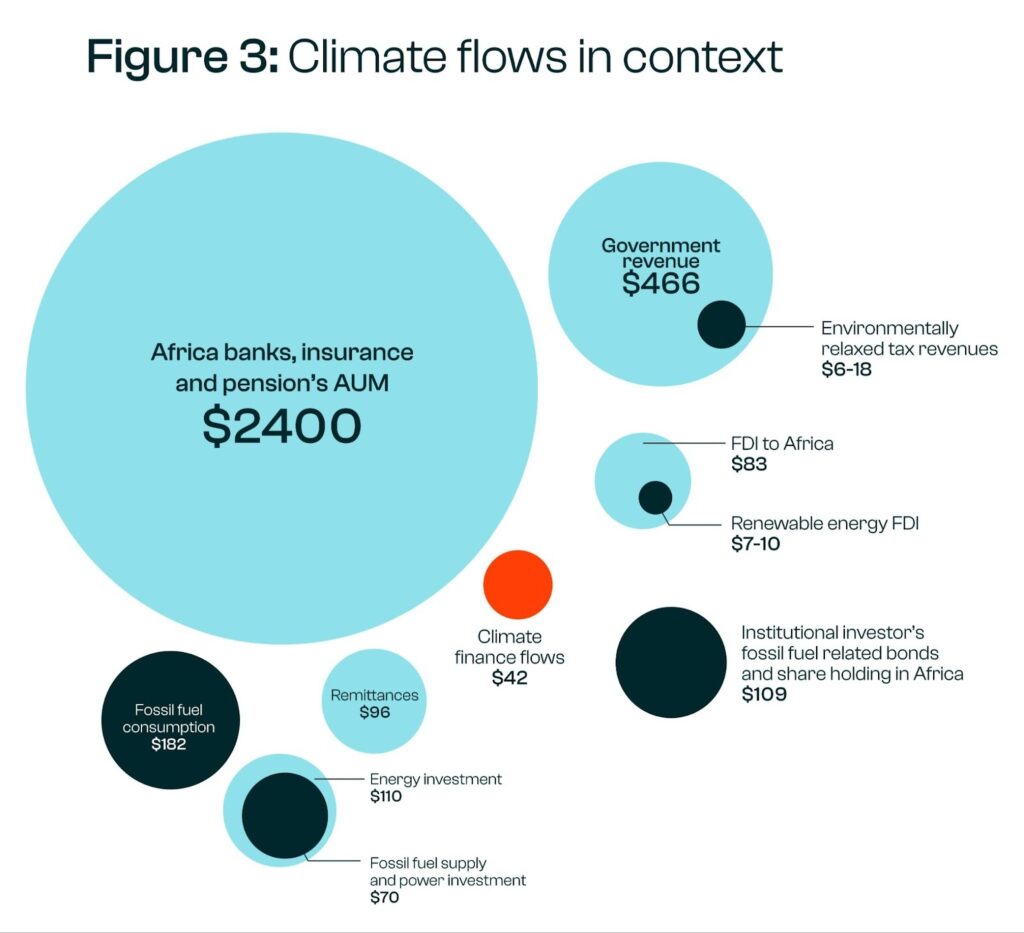

There is also a data and narrative problem. In today’s Reuters report, The Nature Conservancy’s Africa director said the continent receives just 1% of global climate financing. CPI’s broader climate-finance tracking, however, puts Africa’s share at 3.3% in 2021/22. Those numbers do not sit neatly together, and that discrepancy should not be ignored. It may reflect differences in definitions, data coverage, or what exactly is being counted. But analytically, the key point still holds: by any credible estimate, Africa is receiving far less climate finance than its needs and exposure would justify. The disagreement is over the magnitude of underfunding, not its existence.

A second concern is governance. Debt-for-nature swaps work best when the monitoring architecture is credible, the conservation commitments are specific, and the fiscal benefits are clear to citizens and investors. Gabon’s deal survived political upheaval, and Reuters reported today that the country remains committed despite the instability that followed the 2023 transaction. That resilience is encouraging, but it also highlights the risk. These deals rely on long time horizons, institutional continuity, and legal durability. If any of those weaken, the structure can become politically controversial, especially if citizens feel that conservation obligations are being rigidly enforced while broader fiscal pain remains unresolved.

Still, dismissing the instrument would be just as shallow as romanticising it. The better view is that debt-for-nature swaps belong in a financing toolbox, not on a pedestal.

They will not substitute for concessional climate finance, domestic revenue reform, stronger debt management, or deeper multilateral support. But they can create targeted fiscal space in countries where debt costs are high, ecological assets are globally significant, and conventional climate funding remains inadequate. In that sense, they are less about solving African debt and more about changing how part of Africa’s financing gap gets addressed. That is a narrower claim, but it is also a more defensible one.

This new round of African negotiations merits serious attention because it reflects both realism and innovation. It is grounded in realism, given the severity of debt pressures, the persistent shortfall in climate financing, and the constraints facing public budgets across the continent. At the same time, it is innovative in its attempt to reposition natural capital from a vulnerable asset into a viable financing instrument.

Should one of the three deals reach closure in 2026, the true measure of success will not lie in the announcement itself, but in whether the transaction delivers a meaningful reduction in financing costs, safeguards credible ecological assets, and establishes a model that other African governments can adapt without ceding excessive value to intermediaries and transaction costs. That is the standard against which this development should be evaluated.